Are There Limits to Salary Sacrificing?

In this article we’ll walk through the below four (4) points and unpack if extra contributions to your superannuation is worth while.

What are the Different Superannuation Contributions

Benefits to Salary Sacrificing and Contributions

How Much ($) Can I Contribute to My Super

Contribute Even More..?

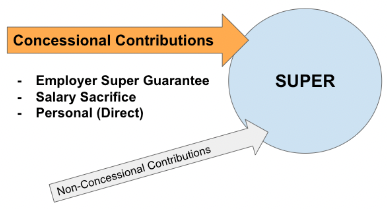

1) What are the Different Superannuation Contributions

There are two types of contributions you can make to your superannuation which are one, concessional contributions and two non-concessional contributions. In todays article we’ll only cover the concessional contributions. Which include the employer super guarantee, salary sacrifice or any personal contributions.

2) Benefits to Salary Sacrificing and Contributions

The benefit for salary sacrificing is the money under concessional contributions is tax at a rate of 15%. This is much lower than your personal income tax rate. So, if you are going to invest for your retirement this is a compelling reason to invest into your superfund!

Example: 100k salary with an average tax rate of 25% (marginal tax rate of 34.5%) you’ll be able to invest 10% more using the Concessional Contribution into your super!

3) How Much ($) Can I Contribute to My Super

With this reduced tax rate you might be tempted to think you can salary sacrifice any amount you wish. However, there are some limitations. The concessional contributions has an annual cap of $27,500. Note this includes your super guarantee from your employer, plus salary sacrifice and any other personal contributions.

An example of this can be seen below, showing that you’d have up to $16,500 available to salary sacrifice.

4) Contribute Even More..?

Lastly we’ll look at if you can contribute even more. The good news is that if you haven’t made any personal contributions or done any salary sacrificing you may be eligible for the ‘carry-forward rule’.

The Carry Forward rule allows you to carry forward any unused portion of the concessional contribution cap for a rolling 5-year period - beginning from the 2018/19 financial year.

An important note, is that you can only utilise unused carry-forward amounts if your super balance was below $500,000 on the 30 June of the previous financial year. If it was higher, you won’t be able to use the carry-forward amount for concessional contributions, but can use the annual cap of $27,500.

Tip: Good to think about any bonuses, or pay rises and how this may affect your limits and when might be best for you to make concessional contributions.

In summary, the concessional contributions scheme is there by the government to incentivize you to save for retirement and build that nest egg. Even if you’re in your earning years in your career or close to retirement this can be a key part of your strategy.

Until next time,

IMPORTANT DISCLAIMER

York Wealth Management Pty Ltd ABN 46 605 610 679 is an Corporate Authorised Representative of Samuel Allgate Investments Pty Ltd AFSL No. 420170; Financial Adviser Authorised Representative Number 001007979.

This article has been prepared without taking into consideration any investor’s financial situations, objectives or needs. Accordingly, before acting on the advice in this article, you should consider its appropriateness to your financial situation, objectives and needs. Every reasonable effort has been made to ensure the information provided is correct, but we cannot make any representation nor warranty as to the accuracy, completeness or currency of that information. To the extent permissible by law, no responsibility for any errors or misstatements is taken, negligent or otherwise. SAI or its authorised representatives may also receive fees or brokerage from dealing in financial products, see the Financial Services Guide for information about the services offered available at York Wealth Management.